In the Pacific Northwest, waiting to save up every dollar for a new roof is often more expensive than financing one today. While you wait for your savings to grow, Shoreline's relentless rain can turn a small shingle issue into a costly structural disaster. You shouldn't have to choose between your financial stability and a dry home. We know the high cost of living in the Seattle area makes a large upfront payment feel out of reach for many families. It's stressful to worry about your attic every time the clouds turn grey.

This guide shows you how to protect your property with the best roof financing options shoreline offers in 2026. You'll learn how to secure manageable monthly payments and fast approval to stop active leaks before they spread. We'll explain why federal energy-efficient tax credits expired on January 1, 2026, and how to navigate the Shoreline eTRAKiT portal for required building permits. You will also discover the modern loan types that help you install a high-quality roof built to last 30 years or more, ensuring your peace of mind throughout the next decade of Washington winters.

Key Takeaways

- Stop structural rot and preserve your cash flow by understanding why financing is a strategic move for Shoreline homeowners.

- Compare the fastest roof financing options shoreline residents can use to kick off their projects without waiting years to save.

- Get your paperwork ready with our 2026 checklist for credit scores and income verification to ensure a smooth approval process.

- Learn how to spot "zero interest" traps and hidden fees to ensure your monthly payments stay low and manageable.

- See how transparent, custom payment plans from local experts provide the financial flexibility your family needs.

Why Financing is a Smart Move for Shoreline Roofs

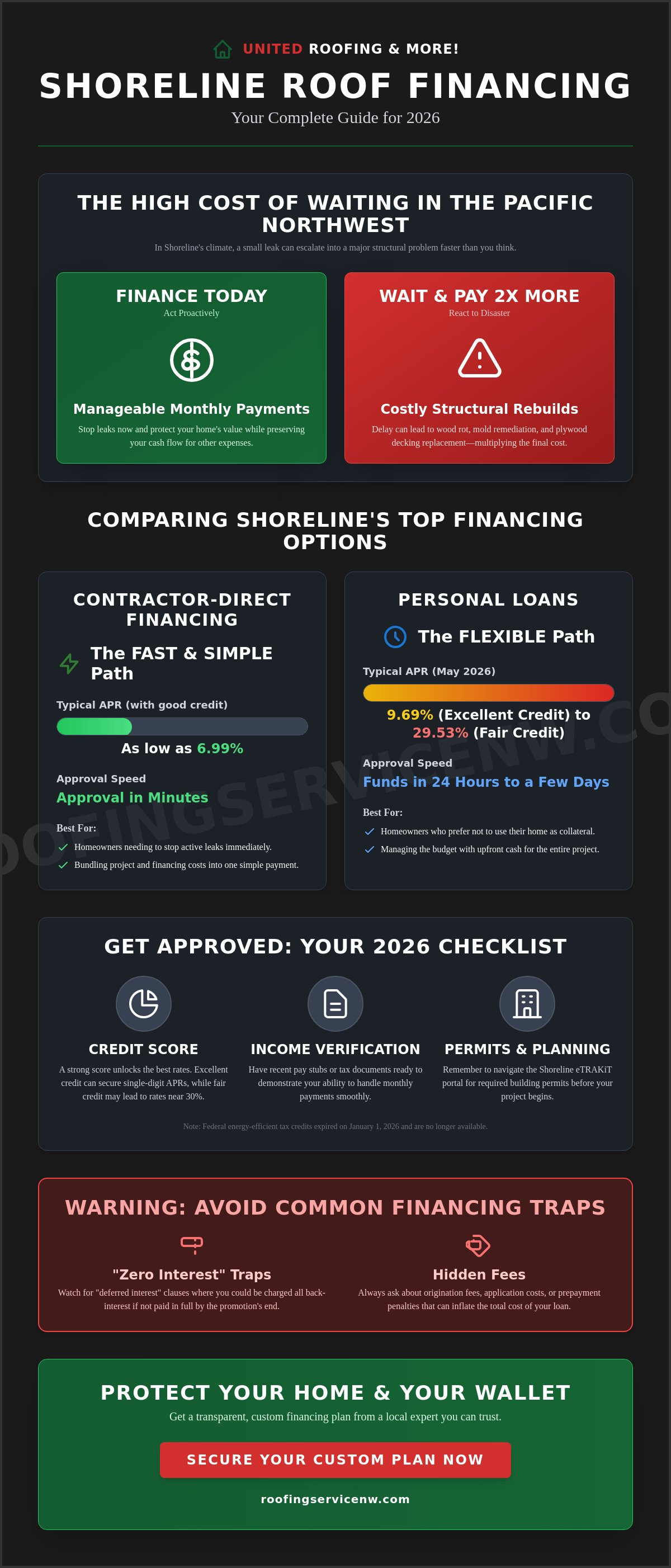

Shoreline's weather doesn't wait for your bank account to catch up. In the Pacific Northwest, rain and moss are constant threats to your home's integrity. Delaying a roof replacement often leads to structural rot that costs twice as much to fix down the road. By exploring roof financing options shoreline homeowners can protect their investment immediately. You keep your cash flow steady for other local living expenses while stopping leaks in their tracks. It's about being proactive rather than reactive.

A new roof adds significant value in Shoreline's competitive housing market. Buyers in 2026 look for durability and modern aesthetics like matte black or charcoal finishes. Financing allows you to upgrade to premium, moss-resistant shingles that standard budgets might miss. This isn't just a simple repair. It is a strategic upgrade for your home's equity. Many homeowners also investigate an FHA insured loan to help fund these essential property improvements when they want government-backed security.

The True Cost of Delaying a Roof Replacement

Small leaks during a Shoreline winter quickly escalate into expensive mold remediation. When water finds its way inside, it doesn't stay in the attic. Moisture trapped under shingles damages plywood decking and creates a breeding ground for wood rot. This compromise to your home's skeleton is dangerous and expensive to fix. Choosing to finance today is a smart financial move. It's far cheaper to pay a low monthly interest rate than to pay for a full structural rebuild in two years. We help you secure the funds needed to stop the damage before it spreads to your ceilings and walls.

Shoreline Weather and Your Roof's Lifespan

Constant humidity and falling Douglas fir debris accelerate roof decay in our region. These needles trap moisture against the surface, which leads to early shingle failure and heavy moss growth. Modern 2026 roofing technologies offer superior protection against this unique PNW climate. Using roof financing options shoreline lets you afford the highest master roofing standards available today. You get a high-quality roof installation that lasts 30 years instead of a quick fix that fails in five. This ensures your peace of mind during the next big storm. Don't let a tight budget force you into a low-quality solution that won't stand up to Shoreline's wind and rain.

Comparing Roof Financing Options in Shoreline

Choosing the right way to pay for your project is just as important as choosing the right shingles. Shoreline homeowners have several distinct paths to fund their repairs or replacements. You can choose between contractor-direct plans, personal loans, or leveraging your home's equity. Each path has different timelines and costs. Understanding these roof financing options shoreline residents use most helps you avoid overpaying for your protection. We want you to feel confident in your decision from the first consultation to the final shingle.

Speed is often a deciding factor, especially when dealing with active leaks during a wet Puget Sound spring. Some options provide cash in hand within 24 hours, while others might take weeks of bank appraisals. Your credit score and available home equity will dictate which route offers the lowest monthly payment. It's about finding the balance between immediate relief and long-term financial health. We lead with transparency to help you navigate these choices without the stress of hidden terms.

Contractor-Direct Financing vs. Personal Loans

Contractor financing is often the fastest way to start a project. If you have an active leak, speed is your best friend. Many local companies offer rates starting as low as 6.99% APR for qualified customers. These plans simplify the roof replacement process by bundling the material and labor costs into one monthly bill. You often get approval in minutes rather than days. This is a "no-nonsense" approach that keeps your project moving forward without bank delays.

Personal loans are another popular unsecured option. They don't require you to put up your house as collateral. As of May 2026, the average APR for a personal loan with excellent credit is 9.69%. If your credit score is in the "fair" range, you might see rates closer to 29.53%. It is helpful to review the official definition of a home improvement loan to understand how these funds are regulated. These loans provide cash upfront, giving you the flexibility to manage your budget your way. If you aren't sure which path fits your budget, you can explore flexible payment plans with a local expert today.

Using Home Equity in the Shoreline Market

Shoreline property values have remained strong through early 2026. This makes a Home Equity Line of Credit (HELOC) an attractive choice for major exterior renovations. A HELOC allows you to borrow against the value you've already built in your home. These often have lower interest rates than personal loans. However, they can take several weeks to close. You should also consult a professional regarding the tax implications of home improvement debt, as laws can change yearly.

Credit cards are a final option, but use them carefully. They are useful for small repairs or if you can snag a 0% introductory APR for 12 months. If you can't pay the balance before the promo ends, interest rates can skyrocket. For a full installation, a dedicated loan is usually much safer. We prioritize clarity and help you find a solution that keeps your home dry without breaking the bank. Our goal is to provide a high-quality roof that lasts 30 years with a payment plan that fits your life.

How to Qualify for Roofing Financing

Qualifying for a loan doesn't have to be a stressful hurdle. Shoreline lenders in 2026 prioritize transparency and clear communication. They primarily look at your credit history, debt-to-income ratio, and the equity in your home. Having this information ready allows you to move quickly when a leak starts. We focus on helping you understand these roof financing options shoreline requirements so you can secure a dry home without the headache. Preparation is the key to a fast approval.

You need to gather specific documentation before applying. Most lenders require proof of income, such as recent pay stubs or tax returns. They also need verification of property ownership in the Shoreline area. It is also smart to research various roof financing options to see which lenders specialize in home improvements. Getting multiple quotes is your first real step. An accurate estimate ensures you aren't borrowing more than necessary, keeping your monthly payments manageable and fair.

Credit Score Requirements and Fair Credit Options

Your credit score is the biggest factor in determining your interest rate. In May 2026, Shoreline homeowners with excellent credit (800-850) see average APRs around 9.69%. If your score is in the "good" range (670-739), rates typically sit near 21.16%. Many "zero-down" programs require a minimum score of 640. If your credit is less than perfect, don't worry. You can still qualify by offering a larger down payment or using a co-signer. This reduces the lender's risk and can significantly lower your long-term interest costs. We believe every family deserves a safe roof regardless of their credit history.

The Shoreline Application Process

The process moves fast once you have an estimate in hand. Lenders in North King County typically provide approval decisions within 24 to 48 hours. You must ensure your contractor accounts for local requirements, such as the Shoreline building permit fees. For projects valued between $25,001 and $50,000, the city charges a $672 fee for the first $50,000. These costs should be included in your total financed amount. It is also vital to calculate roof pitch and total area accurately. These measurements dictate the material needs and labor hours, which form the basis of your loan application. Once the City of Shoreline eTRAKiT portal clears your permit, your financing is ready to fund the project. This organized approach ensures there are no financial surprises halfway through the installation.

Avoiding Common Financing Pitfalls

Financing your project should provide relief, not a future headache. While looking at various roof financing options shoreline lenders provide, it's easy to get distracted by flashy marketing. Some offers look perfect on the surface but contain restrictive clauses in the fine print. We believe in a no-nonsense approach to your home's protection. Transparency is our priority. You need to know exactly what you're signing before the first shingle is removed. Avoiding these common traps ensures your monthly payment remains a help rather than a burden.

One major pitfall is over-borrowing. It is tempting to add extra home improvements to a roofing loan, but this can lead to unmanageable debt. Stick to what your roof actually needs to stay dry and secure. We recommend focusing your budget on high-quality materials and expert installation. This protects your home's structure without stretching your finances too thin. Keep your focus on the goal: a high-quality roof that lasts 30 years or more.

Understanding Deferred Interest Plans

Many homeowners are drawn to "12 months same as cash" offers. These are often deferred interest plans rather than true 0% interest loans. Deferred interest means that if you don't pay the entire balance within the promotional period, the lender charges you for all the interest that would have accrued from day one. This results in a massive interest charge hitting your account on month thirteen. It's a common trap that can erase your savings in a single day. To avoid this, always have a clear plan to pay off the balance before the clock runs out. If you can't guarantee a full payoff, a standard low-interest loan is usually a safer, more predictable path for Shoreline families.

Comparing Total Cost vs. Monthly Payment

Don't focus solely on the monthly bill. A very low monthly payment often indicates a long loan term, sometimes stretching to 144 or 240 months. While this keeps your current budget steady, you might end up paying double the original cost of the roof in interest over time. Always ask for the total "cost of credit" to see the big picture. You should also verify that your contract has no prepayment penalties. This flexibility allows you to pay more when you have extra cash, which shortens the loan and saves you significant money in the long run.

It is also vital that your financed quote includes every essential component for the PNW climate. A cheap estimate might leave out the roof drip edge or proper attic ventilation. If you finance an incomplete system, your roof won't last as long as the loan term. Your financing and your warranty must work together to protect your Shoreline property. We ensure your loan covers a complete, high-performance roofing system from the start. If you want a clear, honest breakdown of your project costs, get a transparent roofing quote today.

Financing Your Project with United Roofing & More!

United Roofing & More! understands that a new roof is a significant investment for Shoreline families. We don't just provide roofing; we provide financial peace of mind. Our team offers flexible payment plans tailored specifically for Puget Sound homeowners. We believe everyone deserves a safe, dry home, regardless of their current cash on hand. By exploring the best roof financing options shoreline has to offer through our partnership, you can start your project today. We lead with a no-nonsense dialogue about costs and credit. This ensures you never feel overwhelmed by the process.

Searching for roof financing near me often leads to confusing bank forms and long wait times. We've streamlined our approval process to get you answers in minutes. This speed is essential when Shoreline's rain is actively damaging your home. Our high-quality workmanship is now more accessible than ever. We combine premium materials with financial solutions that fit your monthly budget perfectly. We are ready when you are.

Our Commitment to Financial Transparency

Transparency isn't just a buzzword for us. It's how we do business every day. We walk you through every single line item in your roofing estimate. You'll see the exact cost of materials, labor, and Shoreline permit fees. As a locally owned contractor, we value long-term trust over high-pressure sales tactics. Our "no-pressure" approach means we provide the facts and let you make the best choice for your family. We keep you informed throughout the entire service process. This clarity is our core promise to the community we serve. We prioritize your peace of mind above all else.

Start Your Shoreline Roof Replacement Today

Your journey to a secure home begins with a simple conversation. You can schedule a complimentary diagnostic and financing consultation at your convenience. During our first visit to your Shoreline home, we'll perform a thorough inspection of your current roof. We identify active leaks, moss growth, and structural weaknesses. After the inspection, we'll sit down with you to discuss our findings and your financial goals. We make the barrier to entry low so you can protect your property immediately. It's time to stop worrying about the next storm. Get your free estimate and explore financing options now!

Take Control of Your Home's Future and Your Budget

Shoreline's rain doesn't pause for a perfect financial moment. You've learned how delaying a replacement leads to structural rot and why 2026 is the year to act. Proactive financing is your best tool to prevent expensive emergency repairs down the road. It is a smart, strategic investment in your property's long-term value. Choosing a plan today ensures your home stays dry through every Pacific Northwest storm.

United Roofing & More! is locally owned and operated in the PNW. We provide professional workmanship guaranteed to withstand our unique climate. With flexible payment plans for all budgets, we make it easy to find the right roof financing options shoreline homeowners need to stay dry. We lead with transparency and honesty in every consultation. Our goal is to lower the barrier to entry so your family can enjoy a safe, high-quality roof without the stress of a massive upfront cost.

Don't let a small leak turn into a major disaster. Our team is ready to help you secure a high-quality roof with a payment plan that fits your life perfectly. Secure your Shoreline home with affordable roof financing today! We look forward to protecting your home and providing the peace of mind you deserve for the next 30 years.

Frequently Asked Questions

What is the typical monthly payment for a new roof in Shoreline?

Your monthly payment depends on the total project cost, your interest rate, and the length of your loan term. Most homeowners choose terms between 60 and 120 months to keep payments manageable. For example, a loan with a 9.69% APR will have a much lower monthly requirement than one at 21.16%. We provide clear, transparent breakdowns during your consultation so you can pick a payment that fits your monthly budget perfectly.

Can I get roof financing in Shoreline with a low credit score?

Yes, options exist for various credit profiles. While the best rates go to those with scores above 740, lenders in 2026 offer programs for "fair" credit scores between 580 and 669. These loans often carry higher interest rates, sometimes reaching 29.53%. You might also consider a co-signer or a larger down payment to improve your approval odds. We work with you to find a supportive partner that values your home's safety over a single number.

Are there any zero-interest roofing financing options available in 2026?

Some local contractors offer 0% interest promotional financing for 6 to 12 months to qualified customers. These are excellent roof financing options shoreline families use to pay off their projects quickly without extra costs. Always verify if the plan uses deferred interest. If you don't pay the full balance before the promotion ends, you could be charged for all the interest that would have built up from the start date.

How long does it take to get approved for roofing financing?

Contractor-direct financing is the fastest route, often providing an approval decision in minutes. You can typically apply right from your kitchen table during an estimate. Traditional bank loans or Home Equity Lines of Credit take longer, usually requiring two to four weeks for processing and appraisals. If you have an active leak and need to start your roof installation immediately, direct financing is your best choice for speed.

Is it better to use a HELOC or a personal loan for a roof replacement?

A HELOC is often better for lower interest rates if you have significant equity in your Shoreline home. However, it uses your house as collateral and takes longer to fund. Personal loans are unsecured and much faster to secure, though interest rates are generally higher. Choose a personal loan if you need to stop structural damage today and a HELOC if you are planning a major renovation months in advance.

Does roof financing cover the cost of Shoreline building permits?

Yes, your financing package can include all associated costs, including city permits. Shoreline requires a building permit for all roof replacements, with fees based on the project's valuation. For a project valued between $25,001 and $50,000, the fee is $672. We ensure these administrative costs are bundled into your loan so you don't have to pay for them out of pocket before the work begins.

What happens if I sell my home before the roof is paid off?

You typically pay off the remaining loan balance using the proceeds from your home sale at closing. A new roof is a major selling point in the competitive North King County market. Homeowners often recoup 60% to 70% of the roof's cost in added home value. This makes your property more attractive to buyers and can lead to a faster sale, effectively helping the roof pay for itself during the transaction.

Can I finance a roof repair instead of a full replacement?

Yes, you can finance significant repairs to address leaks and prevent rot. While many people associate financing with a full roof installation, smaller loans are available for major restoration work. This is a smart way to protect your home's structure when you aren't ready for a total replacement but need professional repairs immediately. We provide the same transparent dialogue and flexible options regardless of the project size.