What if the secret to a successful claim isn't the age of your shingles, but how you document a single windstorm? Most homeowners in Sammamish feel a sense of dread when they look at their roof after a heavy storm. It's frustrating to pay premiums for years only to worry that your claim will be denied or that you'll be stuck with massive out-of-pocket costs. You deserve a process that is transparent and simple.

You can get insurance to pay for roof replacement sammamish by following a professional strategy that focuses on proving a "covered loss" under Washington Administrative Code 284-30. We're here to help you maximize your coverage and minimize financial stress. This 2026 guide breaks down the exact steps to document damage, understand the industry shift toward Actual Cash Value (ACV) policies, and navigate the $269 city permit process to ensure your new roof meets the 2021 Washington State Building Code.

Key Takeaways

- Learn why proving a specific "covered loss" from Sammamish windstorms is the essential first step to triggering your policy coverage.

- Understand the critical difference between ACV and RCV to avoid unexpected funding gaps and high out-of-pocket expenses.

- Discover how to identify subtle "wind uplift" and shingle bruising that insurance adjusters use to justify a full replacement.

- Follow a professional roadmap to get insurance to pay for roof replacement sammamish by securing a detailed damage report before filing your claim.

- Explore how expert documentation and roofing financing can provide peace of mind and financial flexibility throughout the restoration process.

Understanding "Covered Loss" for Your Sammamish Roof

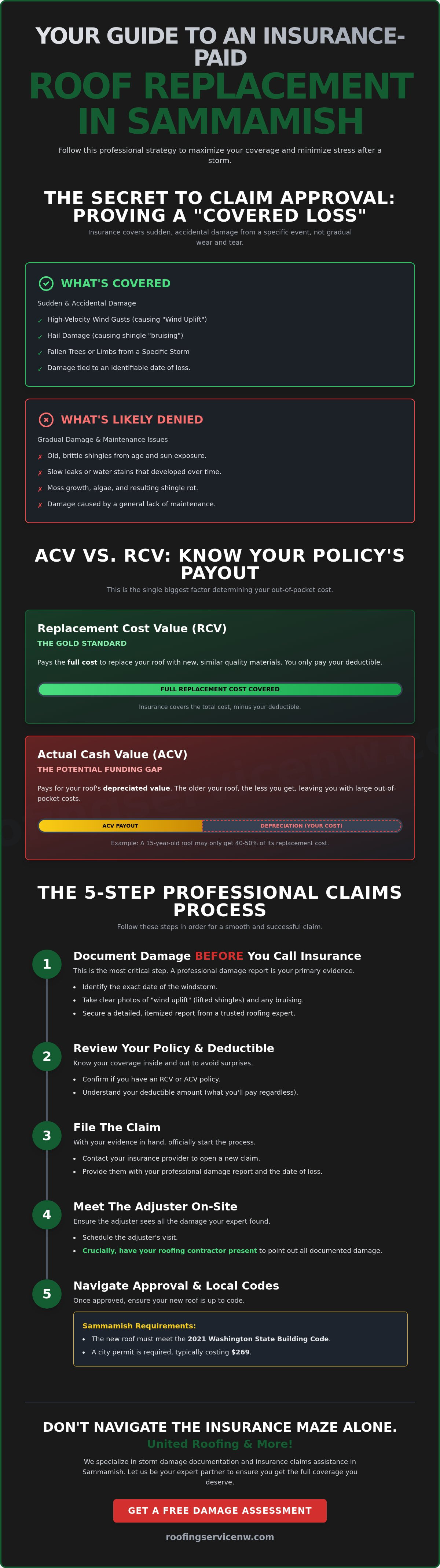

Success in your insurance claim starts with one specific phrase: covered loss. In the world of insurance, a covered loss refers to damage that is sudden, accidental, and caused by a specific, identifiable event. It isn't enough to show that your roof is old or leaking. To get insurance to pay for roof replacement sammamish, you have to prove that a peril like wind, hail, or a fallen tree caused the damage. This distinction is the difference between a fully funded project and a frustrating denial letter.

Sammamish residents often face unique challenges due to our local geography. Our position on the Plateau makes homes more vulnerable to high-velocity wind gusts that don't always hit the lower elevations of King County. When these winds whip across the ridge, they can lift shingles and break the factory adhesive seals. This is structural damage, not just a cosmetic issue. While a few lost granules might look like general wear, the loss of shingle "uplift" resistance is a serious policy trigger. You need to identify the exact date of loss to ensure your claim aligns with local weather records and meets the requirements of Washington Administrative Code 284-30.

A foundational part of Understanding Property Insurance is knowing that policies are designed to protect against sudden accidents, not inevitable aging. Insurance companies look for a clear cause and effect relationship. If a storm hits on a Tuesday and your roof fails on Wednesday, that's a strong case. If your roof has been slowly deteriorating for a decade due to moss growth, the adjuster will likely label it as a maintenance issue. We focus on documenting the "sudden" requirement that adjusters look for in Sammamish to ensure your claim stays on track.

Sudden vs. Gradual Damage: The Insurance Divide

Adjusters are trained to spot the difference between a storm event and neglect. A 20-year-old roof leak is often denied because it's considered gradual damage. Think of it this way: a fallen hemlock limb during a windstorm is a sudden event. In contrast, long-term moss-related shingle rot is a slow process. To maximize your chances, you must show that the damage occurred rapidly. Proper documentation of a specific storm event helps bridge this divide and proves the damage wasn't just a lack of maintenance.

Sammamish Weather Patterns and Policy Triggers

The 2025-2026 storm season brought several high-wind events to the Plateau region that significantly impacted local roofing systems. High-velocity winds are particularly dangerous for asphalt shingles because they create wind uplift. This occurs when wind gets underneath the shingle and breaks the seal. Even if the shingle doesn't blow off, the broken seal means the roof can no longer protect your home according to the 2021 Washington State Residential Code (IRC). While hail is rarer in the Pacific Northwest, it remains a definitive claim trigger because it causes bruising that compromises the shingle's integrity. Identifying these specific triggers is how you get insurance to pay for roof replacement sammamish without the stress of a denial.

ACV vs. RCV: Which Policy Coverage Does Your Home Have?

Your policy type determines your final out-of-pocket costs. If you want to get insurance to pay for roof replacement sammamish, you must first identify if you have an Actual Cash Value (ACV) or Replacement Cost Value (RCV) policy. These two terms might look similar in a thick policy packet. However, they represent a massive difference in your bank account balance after the project is finished. Most modern policies in King County fall into one of these two buckets.

Actual Cash Value is the depreciated value of your roof. Think of it like a used car. The older it gets, the less it's worth. If your roof is 15 years old, the insurance company will deduct 15 years of wear and tear from your payout. This often leaves homeowners with a significant funding gap. Replacement Cost Value is the gold standard. It pays the full cost to replace your roof with brand new materials of similar quality. You still pay your deductible, but the insurance company covers the rest.

Before you file, it helps to review the Step-by-Step: Navigating the Claims Process in Sammamish provided by the state. This ensures you know your rights as a consumer in Washington. Understanding these regulations protects you from common pitfalls during the adjustment phase. It also helps you understand how deductibles are subtracted from your final insurance payout before the work begins.

The Financial Impact of Actual Cash Value

ACV policies are becoming more common in Sammamish as roofs age past the 10-year mark. Carriers use strict depreciation schedules to lower their liability. This means your first check might only cover a fraction of the total cost. It's a tough spot for many local families. If you find yourself facing an unexpected bill because of an ACV policy, exploring roofing financing can help bridge that gap. We believe financial stress shouldn't stop you from protecting your home with a sturdy roof.

How RCV Ensures a Complete Roof Replacement

RCV policies usually involve a two-check process. The first check is the ACV amount. The second check represents the "recoverable depreciation." You receive this final payment only after the work is finished and a final invoice is submitted to the carrier. This system ensures you can complete a high-quality roof replacement without cutting corners. It's the most reliable way to get insurance to pay for roof replacement sammamish in full. We help you document every step so the insurance company has exactly what they need to release those final funds. If you're ready to move forward, we specialize in professional roof replacement that meets all local building codes.

Storm Damage vs. Normal Wear: What Adjusters Look For

Distinguishing between an old roof and a storm-damaged one is the most critical part of your claim. When an insurance adjuster arrives at your Sammamish home, they aren't looking for general age. They are searching for specific, physical evidence of impact or wind force. To get insurance to pay for roof replacement sammamish, you must show that the damage is structural and tied to a specific weather event rather than years of neglect.

Hail damage often appears as "bruising" on the shingle surface. These are small, circular indentations that feel soft to the touch, similar to a bruise on an apple. This impact knocks away the protective granules and exposes the underlying asphalt to UV rays. Wind damage is more common on the Plateau. High-velocity gusts create "wind uplift," which breaks the factory seal and leaves a permanent crease across the shingle tab. Adjusters also pay close attention to the flashing and the roof drip edge. If these components show signs of being pried up by wind, it provides strong evidence for a covered loss.

Age is the number one reason adjusters deny roof replacement claims. Insurance is designed to cover accidents, not the natural end of a product's lifespan. If your shingles are simply brittle and losing granules due to time, the carrier will categorize it as "wear and tear." We focus on finding the specific storm-related triggers that override the age factor. Proving a specific date of loss is the best way to move past the age objection and secure the funding you need.

Signs of Wind Damage on Asphalt Shingles

Keep an eye out for missing shingle tabs or sections that look "lifted." Even if the shingle is still attached, a broken seal is a major problem. During our long, wet PNW winters, wind-driven rain gets forced under these loose shingles and sits against the underlayment. Don't just look at the roof from the ground. Check your attic for sudden spots of light or new water stains on the rafters after a big storm. These internal signs often prove that the external roofing system has failed due to wind pressure.

The "Wear and Tear" Trap

Mechanical damage is a common pitfall that leads to claim denials. This includes scuffs from heavy foot traffic or scratches from overhanging branches. In our community, moss growth is another significant factor. While thick moss looks like it's damaging the roof, insurance companies view it as a maintenance issue. It is never a covered loss. Adhering to master roofing standards requires us to clearly distinguish between these maintenance items and actual storm impact. We document the difference professionally to help you get insurance to pay for roof replacement sammamish while avoiding the "wear and tear" trap.

Step-by-Step: Navigating the Claims Process in Sammamish

Filing a claim for a new roof feels overwhelming. Most homeowners think their first call should be to their insurance agent. However, that isn't always the best path. You need a clear, chronological strategy to get insurance to pay for roof replacement sammamish without unnecessary delays. Following a specific order of operations ensures you don't miss small details that lead to big payouts. It keeps the process organized and keeps you in control of your home's protection.

Success depends on five clear steps. First, get a professional inspection. Second, review your policy for specific wind or hail deductibles. Third, file the claim and provide your roofer’s detailed documentation. Fourth, meet with the insurance adjuster alongside your contractor to ensure all damage is seen. Finally, review the final scope of work and start the replacement process. This structured approach removes the guesswork from a complex situation.

Why the Inspection Comes Before the Claim

Calling your insurance company before an inspection is a common mistake. If an adjuster finds no damage, you've filed a "frivolous claim." These stay on your insurance record and can raise your premiums even if you receive zero dollars. You need photo evidence of the damage before the adjuster ever steps foot on your property. A contractor’s report acts as a baseline for the adjuster. This documentation proves the damage exists and forces the insurance company to address specific structural issues from the start. It's about being prepared with facts rather than just a suspicion of damage.

Meeting the Adjuster: A Collaborative Approach

Never meet the insurance adjuster alone. Having your roofing professional present ensures that no subtle damage is overlooked during the walk-through. Adjusters are often on tight schedules and might miss "wind uplift" or creased shingles. We speak their language and can point out specific issues that trigger a full replacement. We also ensure that the "Scope of Loss" includes essential local requirements. For example, the City of Sammamish requires a $269 permit fee for single-family residential re-roofs in 2026. All work must also comply with the 2021 Washington State Residential Code (IRC). If these costs aren't in the initial estimate, you'll be stuck paying for them yourself. If you're ready for an expert second opinion on your storm damage, contact us for a professional roof installation consultation today.

Handling discrepancies in the estimate is part of the process. If the insurance company’s quote is too low, we provide the necessary documentation to justify a supplement. This ensures the final payout covers the true cost of a high-quality roof that meets every safety standard. We prioritize clarity and open dialogue to make sure your claim is handled fairly from start to finish.

United Roofing & More!: Your Local Claim and Financing Partner

United Roofing & More! stands as the leading expert for storm restoration in our community. We understand that the Sammamish Plateau presents unique challenges for every homeowner. High winds and heavy rain require a specific approach to documentation and repair. Our team takes a "no-nonsense" stance when it comes to identifying insurance-worthy damage. We don't just look for leaks. We look for the structural failures that adjusters need to see to approve a full project. Our goal is to alleviate your stress by acting as a supportive partner throughout the entire process.

We know exactly how to get insurance to pay for roof replacement sammamish by providing the technical proof carriers demand. Trust is built through transparency and results. We lead with our professional credentials and a commitment to keeping you informed. Whether you are dealing with a recent windstorm or a complex hail claim, we ensure your home is restored to the highest standards. We prioritize your peace of mind and the long-term safety of your property.

Expert Documentation and Adjuster Communication

Our process involves creating detailed reports that insurance companies respect. We have a strong local presence in Sammamish and across King County. This means we understand the specific weather patterns that hit our ridge. When we meet with an adjuster, we don't just point at shingles. We explain the technical aspects of the job. We can accurately calculate roof pitch and geometry to ensure material counts are precise. This level of detail prevents underpayment and ensures the scope of work covers everything required by the 2021 Washington State Building Code.

Flexible Financing for Out-of-Pocket Costs

Sometimes a claim is only partially approved, or you're stuck with a high deductible. This is common with Actual Cash Value (ACV) policies that leave a funding gap for older roofs. We offer roofing financing as a secondary solution to ensure you don't have to delay essential work. Our application process is simple and designed to provide financial flexibility when you need it most. We believe every family deserves a safe roof regardless of their immediate insurance payout. If you're worried about a denied claim or high costs, we can help you find a path forward. Contact United Roofing & More! for a free claim-readiness inspection.

Secure Your Sammamish Home Today

Your roof is the most important shield against the intense weather patterns of the Sammamish Plateau. We've explored how proving a specific "covered loss" is the foundation of every successful claim. It's also vital to understand your policy type and ensure your contractor is present for the adjuster's inspection. These steps ensure you don't fall into the common trap of being denied for general wear and tear. You can get insurance to pay for roof replacement sammamish by providing the high-level documentation that carriers require.

United Roofing & More! is here to serve as your locally owned King County expert. We are certified for high-wind PNW installations and offer dedicated roofing financing to bridge any funding gaps. We believe in transparency and hard work to protect our neighbors. Our team is ready to help you navigate the $269 permit process and ensure your home meets all 2021 building codes. Let's work together to restore your peace of mind and your home's integrity.

Get Your Free Sammamish Roof Inspection Today!

Frequently Asked Questions

How much does insurance typically pay for a roof replacement in Sammamish?

Insurance typically pays the full cost of replacement minus your deductible, provided you have a Replacement Cost Value (RCV) policy. If you have an Actual Cash Value (ACV) policy, they pay the depreciated value based on the age of your shingles. According to 2026 data, the average roof replacement in Sammamish is approximately $25,942. Your specific payout depends on your policy limits and the extent of the "covered loss" documented by your contractor.

Can I get a new roof if my claim was denied for "normal wear and tear"?

You can still get a new roof through a re-inspection if you can prove that a specific storm event caused the damage. Adjusters often default to "wear and tear" when they don't see immediate, obvious impact from the ground. We specialize in finding "wind uplift" and shingle bruising that adjusters often miss during their initial walk-through. If you can provide a professional report showing storm damage, you can often get insurance to pay for roof replacement sammamish even after an initial denial.

Will my insurance premiums go up if I file a roof damage claim?

Filing a single "act of God" claim, such as wind or hail damage, typically does not cause an individual premium spike in Washington. However, insurance companies may raise rates for an entire zip code if a major storm affects many homes in the Sammamish area. It is always best to check with your specific agent regarding your policy’s history and local rate adjustments. We recommend having a professional inspection first to ensure the claim is worth filing.

How long do I have to file a claim after a storm in King County?

Most insurance policies require you to file a claim within 30 days of discovering the damage, but some allow up to one year. Washington Administrative Code 284-30 governs these timelines and ensures consumers are treated fairly. It is crucial to act quickly after a storm to ensure the damage is clearly tied to a specific weather event. Waiting too long can lead to a denial based on "gradual damage" or a lack of maintenance.

What happens if the insurance estimate is lower than the contractor’s quote?

You can request a "supplement" if the insurance estimate is lower than the actual cost of materials and labor. This is a common part of the process where your contractor provides additional documentation or invoices to justify the higher price. We ensure the estimate includes necessary local costs, such as the $269 Sammamish permit fee and requirements from the 2021 Washington State Residential Code. This ensures your final payout covers the true cost of a professional installation.

Is it illegal for a roofing contractor to pay my insurance deductible?

Yes, it is illegal in Washington for a contractor to pay, waive, or "absorb" your insurance deductible. Doing so is considered insurance fraud and can lead to serious legal consequences for both the homeowner and the contractor. Instead of looking for deductible waivers, many homeowners use roofing financing to manage their out-of-pocket expenses. This allows you to maintain a legal and transparent claim process while keeping your project affordable.

Does homeowners insurance cover roof leaks caused by moss or algae?

Homeowners insurance generally does not cover roof leaks caused by moss, algae, or lack of maintenance. These issues are considered "gradual damage" rather than a "sudden and accidental" event. To get insurance to pay for roof replacement sammamish, the leak must be the direct result of a covered peril like a fallen tree or high-velocity wind gusts. Regular maintenance is the homeowner's responsibility and is key to ensuring your policy remains valid for future claims.

Can I replace my roof myself and keep the insurance money?

You can technically perform the work yourself, but you will only receive the portion of the money that covers materials and your own labor at a significantly lower rate. If you have an RCV policy, the insurance company will not release the "recoverable depreciation" unless they receive a final invoice from a professional contractor. Most mortgage lenders also require professional installation to protect the collateral of your home and ensure the work meets local safety codes.